May PCE Inflation Puts Fed Rate Hike Risk Back in Front of Markets

The Fed's preferred inflation gauge rose 4.1% in May, while income and consumer spending each climbed 0.7%. That combination matters for investors, borrowers and homebuyers because it keeps rate-hike risk alive even if falling oil prices cool part of the shock.

Pending review

This article is in WireNorth's review workflow and may include AI-assisted research, drafting, or formatting. Pending articles are not eligible for search indexing until editor review is complete.

Editorial standards

Why it matters

The Fed's preferred inflation gauge rose 4.1% in May, while income and consumer spending each climbed 0.7%. That combination matters for investors, borrowers and homebuyers because it keeps rate-hike risk alive even if falling oil prices cool part of the shock.

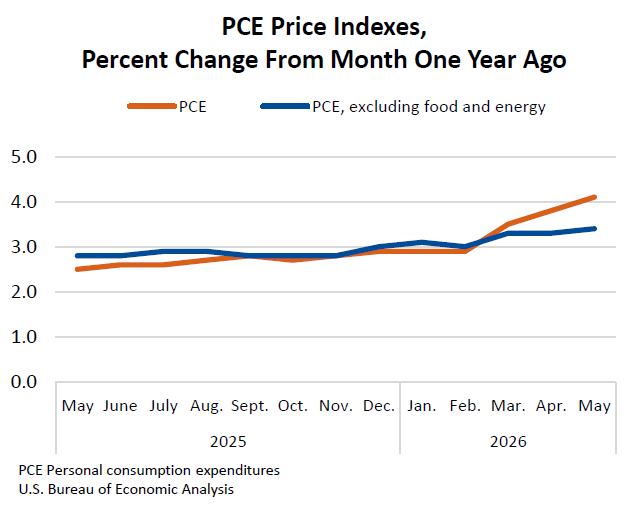

The Federal Reserve's preferred inflation gauge moved back above 4% in May, giving markets a clearer reason to keep rate-hike risk on the table even after oil prices began to retreat.

The Bureau of Economic Analysis said the personal consumption expenditures price index rose 0.4% from April and 4.1% from a year earlier. Core PCE, which excludes food and energy, rose 0.3% on the month and 3.4% from a year earlier. Personal income, disposable personal income and consumer spending each increased 0.7% in May.

That mix is the market story. Inflation was not only hotter because energy prices rose during the Middle East shock. Households were still earning and spending, which means the Fed has less evidence that demand is slowing enough to pull inflation back toward its 2% goal without more policy pressure.

| Indicator | May reading | Why it matters |

|---|---|---|

| Headline PCE inflation | 4.1% year over year; 0.4% month over month, according to BEA | Puts the Fed's preferred inflation measure at roughly twice its 2% goal. |

| Core PCE inflation | 3.4% year over year; 0.3% month over month | Shows underlying inflation remained firm even after excluding food and energy. |

| Consumer spending | Current-dollar PCE rose $156.1 billion, or 0.7%, in May | Signals households were still spending despite higher prices. |

| Real consumer spending | Real PCE increased $43.8 billion, or 0.3% | Shows spending growth was not only a price effect. |

| Personal saving rate | 3.0% of disposable personal income | Leaves a caveat: consumer strength may depend partly on thinner savings cushions. |

| Fed policy range | 3.50% to 3.75% after the June 17 FOMC vote | A steady nominal rate becomes less restrictive if inflation keeps rising. |

Why the May PCE report matters for markets

The immediate reader question is whether this report changes the Fed story. It does not guarantee a rate hike, but it makes a simple rate-cut narrative harder to defend. The Fed held its target range at 3.50% to 3.75% on June 17 and said inflation remained elevated relative to its 2% goal. A week later, BEA data showed headline PCE inflation at 4.1% and core PCE at 3.4%.

The Fed's own June projections had already shifted in a more inflation-conscious direction. Policymakers' median 2026 projection put PCE inflation at 3.6% and core PCE at 3.3%, with the federal funds rate ending the year at 3.8%. The May data landed close to the high side of that inflation problem, not below it.

For stocks and bonds, the second-layer point is that strong nominal growth can be both supportive and uncomfortable. Consumer spending can help corporate revenue, but persistent inflation can keep Treasury yields higher, pressure rate-sensitive sectors and reduce the odds that lower borrowing costs arrive quickly.

Borrowers and homebuyers face a longer wait

The practical effect reaches beyond traders. A higher-for-longer or hike-risk Fed path can keep pressure on mortgage rates, credit-card rates, auto loans and business borrowing costs. That matters for households trying to decide whether to buy a home, refinance debt or wait for rates to fall.

Mortgage-rate data already show the housing market is not getting a clean affordability reset. Freddie Mac reported that the 30-year fixed mortgage averaged 6.49% as of June 25, only slightly above the prior week but still elevated for buyers facing high prices and tight budgets. A hot PCE report does not directly set mortgage rates, but it influences the Treasury-yield and Fed-expectations backdrop that lenders price against.

Banks and lenders are affected in a different way. Higher rates can support net interest income for some institutions, but they can also slow loan demand and increase credit stress for borrowers who need to refinance. That is why inflation data now carries direct consumer-finance consequences, not just market-color value.

The caveat is energy may cool before core inflation does

There is one important limitation. May's headline PCE reading captured a period when energy prices were being pushed higher by Middle East conflict risk. Reuters reported that oil prices had fallen back toward pre-war levels after a preliminary U.S.-Iran peace deal, which could ease part of the headline inflation pressure in later data.

That does not remove the problem. Axios noted that income and spending strength suggest inflation pressure was not exclusively an energy shock. Reuters also reported that services inflation and AI-related business investment are complicating the picture, with memory-chip prices and technology spending feeding into some cost pressures.

The Cleveland Fed's June 26 nowcast points to a possible moderation in headline PCE inflation to 3.90% in June, while core PCE is estimated at 3.43%. Those are forecasts, not official data, but they show the policy challenge: headline inflation may ease if energy cools, while core inflation may remain too high for the Fed to declare victory.

What to watch next

The next major checkpoint is the June Personal Income and Outlays report, scheduled by BEA for July 30. The key question will be whether headline PCE falls with energy prices while core PCE remains sticky, or whether both measures finally move lower together.

Markets should also watch Fed communication ahead of the September 15-16 meeting. Reuters reported that financial markets saw a roughly 80% chance of a September hike after the May inflation release, based on CME FedWatch pricing. That probability can move quickly if June and July inflation, job growth or oil prices surprise.

The final checkpoint is consumer resilience. May spending looked firm, but the saving rate was only 3.0%. If households keep spending while inflation stays high, the Fed's inflation problem persists. If spending slows as savings cushions thin, investors may face a different risk: weaker growth arriving before inflation is fully back under control.

Sources & further reading

- Personal Income and Outlays, May 2026U.S. Bureau of Economic Analysis

- Personal Consumption Expenditures Price IndexU.S. Bureau of Economic Analysis

- Federal Reserve issues FOMC statementFederal Reserve Board

- June 17, 2026: FOMC Projections materialsFederal Reserve Board

- Fed rate hike fears grow as inflation tops 4% in MayReuters via Finance & Commerce

- Hot inflation, strong economy: the Fed's new testAxios

- Inflation NowcastingFederal Reserve Bank of Cleveland

- Mortgage RatesFreddie Mac

Recommended reads

July Minimum-Wage Raises Give Workers a Clear Paycheck Checkpoint

Alaska, Oregon, the District of Columbia, California health care employers and more than 20 local jurisdictions have July 1 minimum-wage changes. The raises are targeted rather than nationwide, but they give covered workers a concrete pay floor to check and give small employers a practical payroll deadline.

Read analysis

New State PBM Rules Put Pharmacy Access Ahead of Quick Drug-Price Promises

States are moving against pharmacy benefit managers with transparency, rebate and reimbursement rules, a change that may help local pharmacies and patients compare costs more clearly even if lower out-of-pocket prices are not guaranteed.

Read analysis